Need money to make money? Strategies to start building wealth

- 6 min read

What we'll cover

-

How to stregthen your savings strategy

-

Determine your risk level tolerance

-

Strategies on how to start building wealth

You’ve heard the adage: You need money to make money. While this common financial advice may sound a little counterintuitive on the surface, the nugget of truth underpinning it is the reason it’s so popular. Wealth can seem like a word that only belongs to those who already have it. The gap between saving and wealth building might feel overwhelming, but generating wealth from scratch is possible with some planning and focus.

Strengthen your savings strategy.

You know how important saving is, but are you doing everything you can to make the most of your nest egg? For instance, making regular automated deposits to a retirement or brokerage account is an excellent step to take, if that's not something you're already doing. Automating your investing is one strategy to employ as you look to grow your wealth.

It’s also possible to have too much in savings. Yes, really! If you have more than six to twelve months’ worth of living expenses in your savings account (the recommended amount for an emergency fund), it might be wise to invest the excess based on your financial objectives, risk tolerance and timeline. Basically, take the time to think about where your money can best serve you.

Make investing a habit.

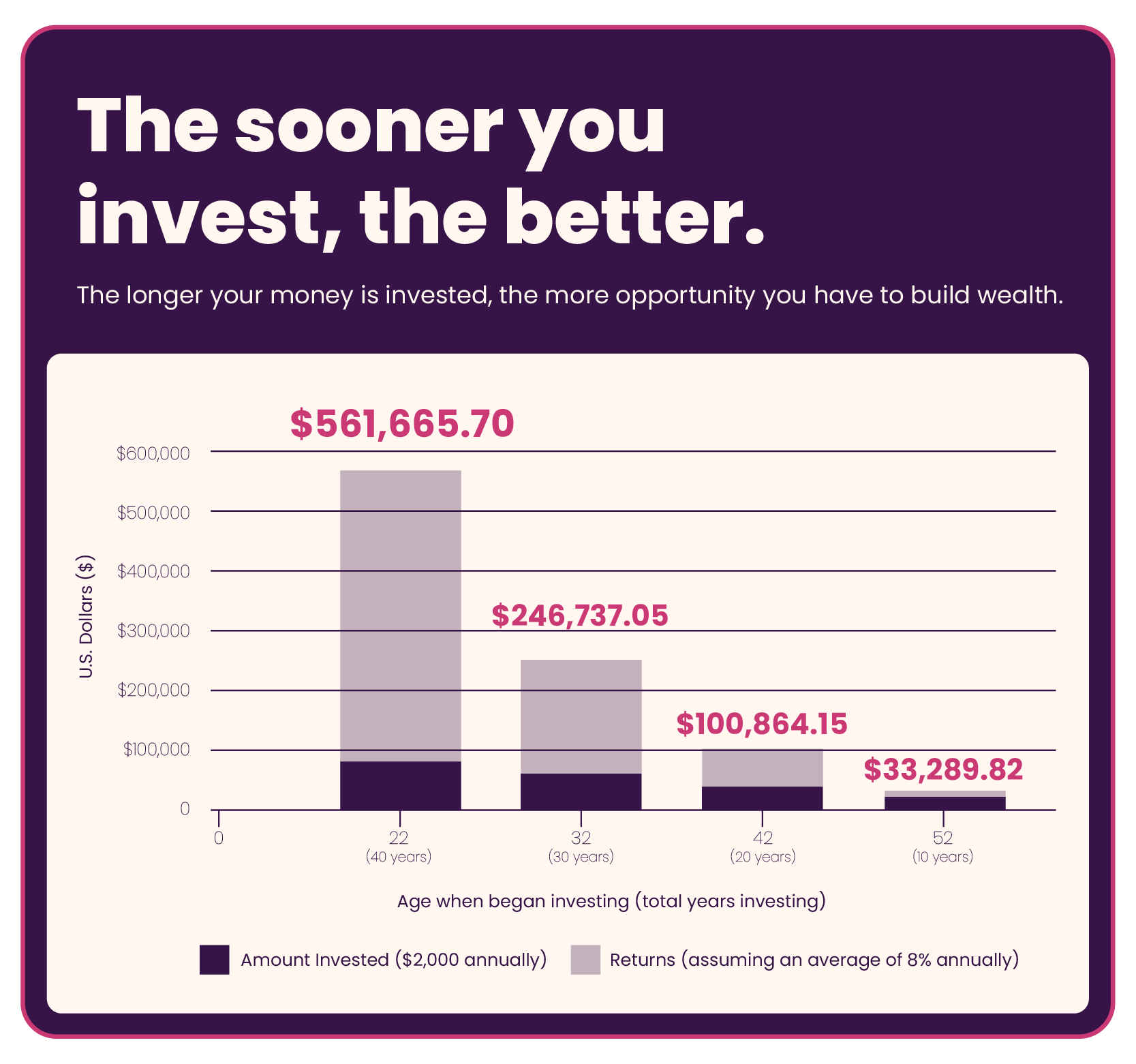

It’s never too early or too late to start investing, and the most important thing is to get started and stay consistent.

With Ally Invest Robo Portfolios , you can start investing with just $100. You probably already know that it pays to begin investing early because of the power of compounding returns. To boost your earning potential even more, consider adding just $50 a month with automated transfers or split your paycheck between your checking account and your investment account when it’s directly deposited to automatically add to your portfolio.

The market can be unpredictable, and you may be concerned about how to ride out the inevitable ups and downs. One popular method to mitigate fluctuations is dollar-cost averaging. By investing equal amounts over regular intervals across time, you can reduce your exposure to volatility and potentially be rewarded for your consistency.

Assess and manage risk.

Now that you’ve decided to invest, you should determine your level of risk tolerance. When it comes to risk and investing, another common axiom holds true: no risk, no reward. Risk is inherent in investing, so when crafting a portfolio, aim to take strategic risks to help you build wealth.

However, the amount of risk that’s right for you is an individual decision and depends on your needs and goals. One important factor in deciding how much risk to take on is your stage of life. If you have many working years ahead of you, you may feel more comfortable taking on more risk. But if you’re hoping to draw on your investments soon, it may be time to dial back your risk level.

You can utilize a multi-pronged approach to determine the ideal level for you. Do your own research as well as check with your employer’s benefits program to see if you have access to financial professionals that can help you assess your preferred level of risk.

Once you establish an appropriate level, you can adjust your investing strategy accordingly. If you find your tolerance is on the lower side, you can take a more conservative approach. Keep in mind that in exchange for less risk, your returns could be lower. Conversely, if you find you have a higher tolerance, you might consider more aggressive tactics.

Regardless of your risk level, diversification is also a key component of your investing strategy. By adhering to another adage — don’t put all your eggs in one basket — you can better balance out your investment portfolio.

A diverse portfolio composed of various securities that align with your investment goals helps protect you from volatility — if one stock goes down, you have others to help soften the impact. Our Robo Portfolios offers a diversified portfolio without the hands-on work, while the tools in our Self-Directed Trading account will help you research your investments and analyze your accounts, so you stay on track.

Different types of securities have unique risk profiles, advantages and disadvantages — all of which you can leverage differently as part of your overall wealth-building strategy:

-

Mutual funds allow you to diversify and access a wider variety of investments than you could afford to buy on your own.

-

ETFs simplify investing by allowing you to diversify without picking individual securities. ETFs typically have lower costs to manage and operate (compared to mutual funds) and may have lower annual taxable distributions as well.

-

Individual stocks are generally riskier and more volatile than mutual funds or ETFs but offer the ability to manage risk more precisely. They are typically more tax efficient, too, if the stock is bought and held (rather than actively traded).

-

Bonds can be used to offset riskier investments in your portfolio and help generate returns during times of volatility.

-

Options offer flexibility and liquidity but can be much riskier than buying individual stocks, bonds or ETFs.

Level up your nest egg.

Eventually, you might be interested in working with a qualified financial advisor to help you elevate your asset management to the next level. Most brokerages have minimum asset thresholds you must meet to work with an advisor — for instance, you can begin working with an Ally Invest Senior Financial Advisor at $100,000 in assets. While $100,000 is a lower entry point than many, if that’s not a good fit for you as you work toward growing your wealth, remember that there are many tools that can help you pursue your goals. Start with the basics and use the strategies above to bring your savings to the next level.

Learning to leverage what you already have is essential to a strong long-term wealth-building strategy. Strengthen your savings strategies, practice consistent investing habits and grow your financial knowledge to help build your nest egg into something that brings you increased financial comfort and confidence.

Read next

Money solutions and strategies sent straight to your inbox.

Tips and tools to help you build your best financial future.