5 signs of a market bottom

LINDSEY BELL • May 13, 2022 • 5 min read

The stock selloff of 2022 feels like it could go on forever.

While it’s hard to call the bottom, one thing we do know is all stock market corrections and bear markets in history have eventually recovered. It can feel painful on the downside, especially when the “R” word is showing up more and more: Recession. Instead of jumping ship, consider looking for signs of when the stock market might find its footing.

There are five telltale indicators Wall Street uses to call a bottom in stocks, and you can learn to use them, too.

1. A VIX spike. The market’s fear gauge is a good place to start when looking for a market bottom. You’ll have an idea of when panic or maximum fear is truly setting in when the Chicago Board Options Exchange’s (CBOE) Volatility Index (VIX) spikes. This index measures the price of options on the S&P 500. Essentially, demand for options increases because people are looking for ways to protect their portfolios, thus the price of those options increases. That’s a sign of rising uncertainty. The gauge hit 35-plus a few times this year and has been above 30 for almost three weeks. However, past bear markets featured moves above 45. The VIX even surged above 80 during both the Great Financial Crisis and the COVID-crash of March 2020. A volatility climax is a signature of market bottoms .

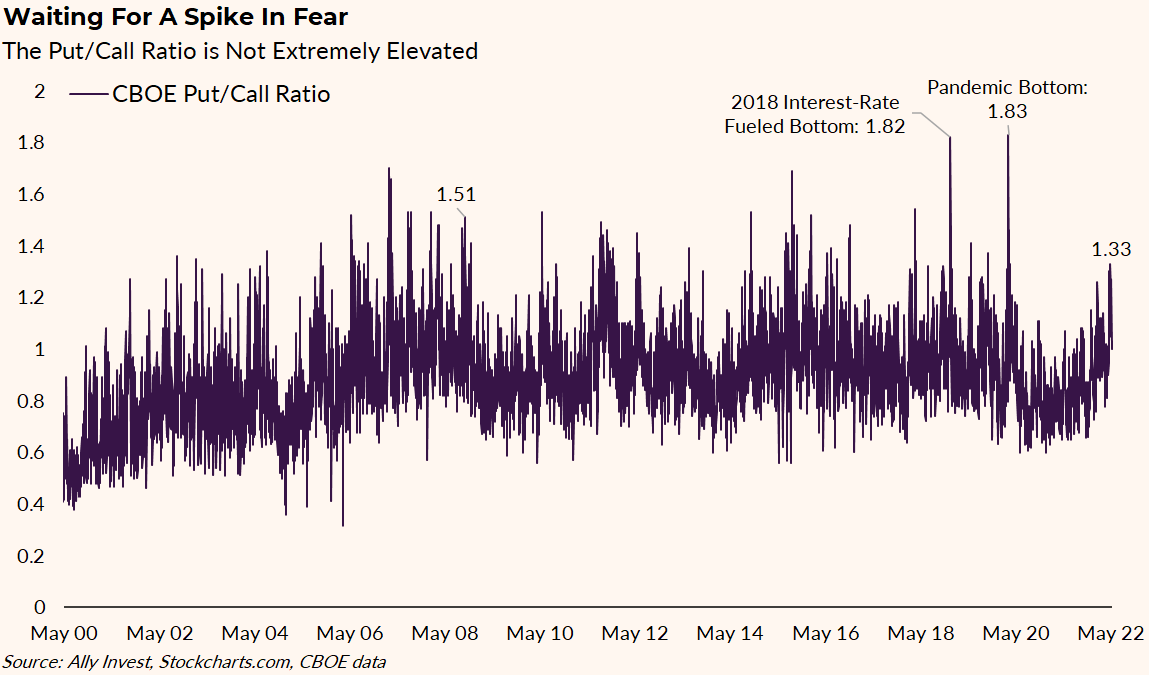

2. Puts sharply outnumbering calls. The options market is full of clues when it comes to market sentiment. In addition to the VIX, the lesser publicized put-call ratio can be another good indicator to watch in volatile times. When put option (puts are bets the market will decline) trading volume exceeds call option (calls are bets the market will rise) trading volume, it tells market analysts that bearish expectations are on the rise. It can be a contrarian indicator when the ratio of daily put volume to call volume rises to, say, 1.50. Put-call spikes to near 1.70 and 1.80 occurred in both the late-2018 downturn and in early 2020. The biggest reading so far this year has only been 1.33. Close, but no cigar.

3. Few stocks trading above key moving averages. Old-school Wall Street traders use the 200-day moving average stock price as the barometer of a long-term trend. For the broad market, when only a handful of S&P 500 stocks are in an uptrend – above their respective 200-day moving average – that suggests significant pessimism is in place. Look for fewer than 20% of equities trading above their 200-day to suggest this. Today, nearly 30% of stocks are above that moving average. It would take an extreme give-up in stocks to match 2009’s washout figure of 1% and 3% in early 2020. Readings of 10% to 15% might suffice for a bottom in the current downturn.

4. A wide difference between risky and safe haven bond yields. The bond market, often called “the smart money,” tells its own story about the future of the economy and stocks. We can gain wisdom from what’s happening based on action in high-quality corporate debt and high-yield junk debt markets. A hallmark of maximum pain and a potential bullish turn in stocks is when rates on risky bonds surge compared to those on safe haven Treasuries. When the yield premium on high-grade corporate bonds rises above 2.50% versus the Treasury yield, and 8% on high-yield fixed income, historically, that’s when too much bankruptcy risk is priced in. Stocks then tend to do well as corporate pessimism subsides. Investment-grade and junk bond yield spreads are currently near 1.40% and 4.50%, respectively.

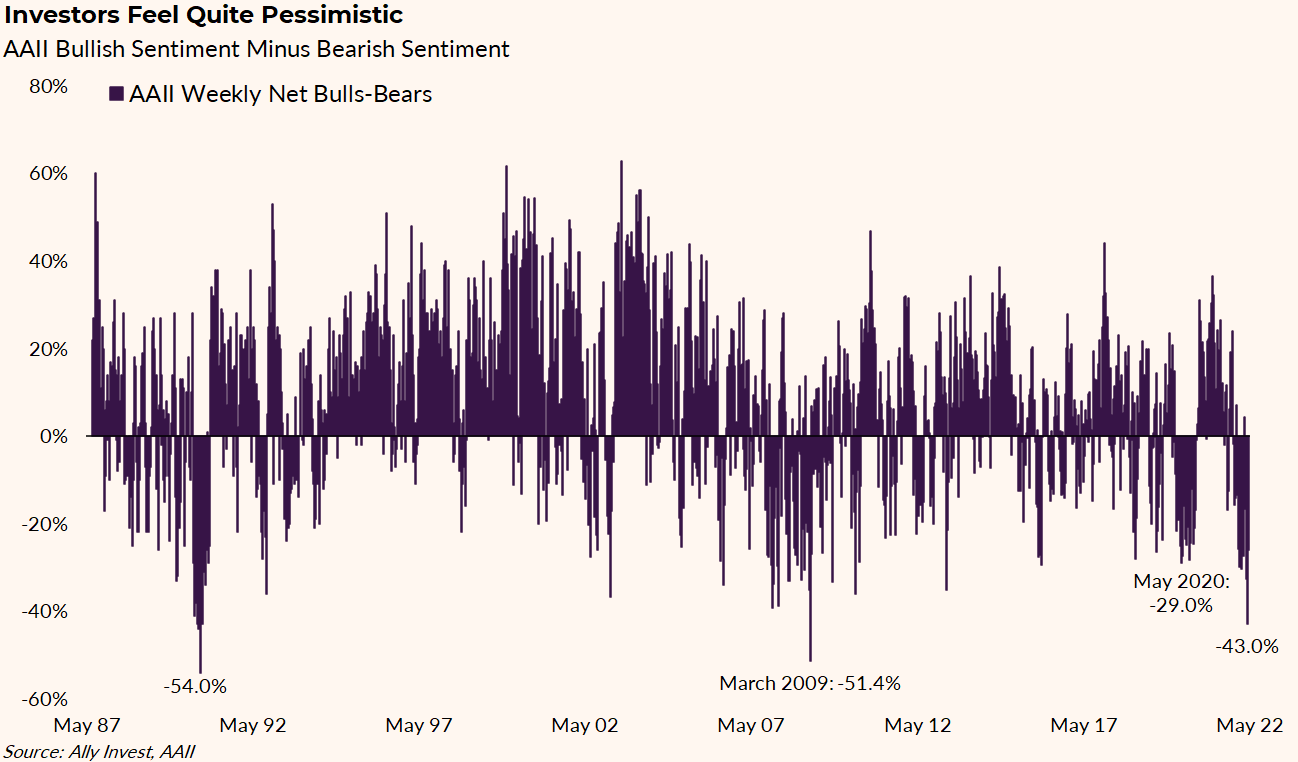

5. Dismal investor sentiment. Our final tool to spot a low in the S&P 500 is simply how investors feel. The American Association of Individual Investors (AAII) publishes a weekly report asking investors where they think the stock market will be in six months. “Bulls” see a higher market while “bears” expect stocks to be lower. When bears outnumber bulls by more than 30%, traders pay attention. 2022 has been particularly bearish as the “net bulls” (bullish percent minus bearish percent) reading hit -43 in late April. This sentiment indicator hints that we could be near a market bottom.

The bottom line

One thing’s certain in financial markets: There is rarely any certainty. That can be quite nerve-wracking when the market is declining, and your money is on the line. Knowing which indicators to watch for as clues into the market’s direction can help provide some level of comfort when the market seems to be doing its own thing.

Four of the five indicators listed above haven’t quite reached extreme levels, which suggests more downside may be ahead of us. However, we may not be far away from the bottom given three of five are approaching extreme levels. It’s often when fear runs highest that the best long-term buying opportunities present themselves. But don’t try to time the market – even the pros have little success doing that.

Lindsey Bell is an award-winning investment professional with a passion for personal finance and more than 17 years of Wall Street experience. Bell’s unique ability to connect the dots between data and real life and craft bite-sized money ideas that people can use and apply stems from her deep background as an analyst, researcher and portfolio manager at organizations including J.P. Morgan and Deutsche Bank. She is known for demonstrating why and how an understanding of all things money improves a person’s finances and overall well-being. An ongoing CNBC contributor, Bell empowers consumers and investors across all walks of life and frequently shares her insights with the Wall Street Journal, Barron’s, Kiplinger’s, Forbes and Business Insider. She also serves on the board of Better Investing, a non-profit focused on investment education.

Read next

Money solutions and strategies sent straight to your inbox.

Tips and tools to help you build your best financial future.