The housing dilemma — should you rent or own?

- 3 min read

What we'll cover

-

The pros and cons of buying vs. renting

-

How appreciation improves the value of homes

-

What to consider when deciding to rent or own

Is it better to rent or to buy a home? The decision to rent or buy affects your wallet in the short term — and your financial future.

To determine the cost difference between renting and buying, you need to consider a number of factors, including: the location, purchase price of home, down payment amount, mortgage terms, how long you plan to live there and the cost of renting a similar home.

But cost isn't the only thing to keep in mind. Consider the advantages and disadvantages to decide what to do next.

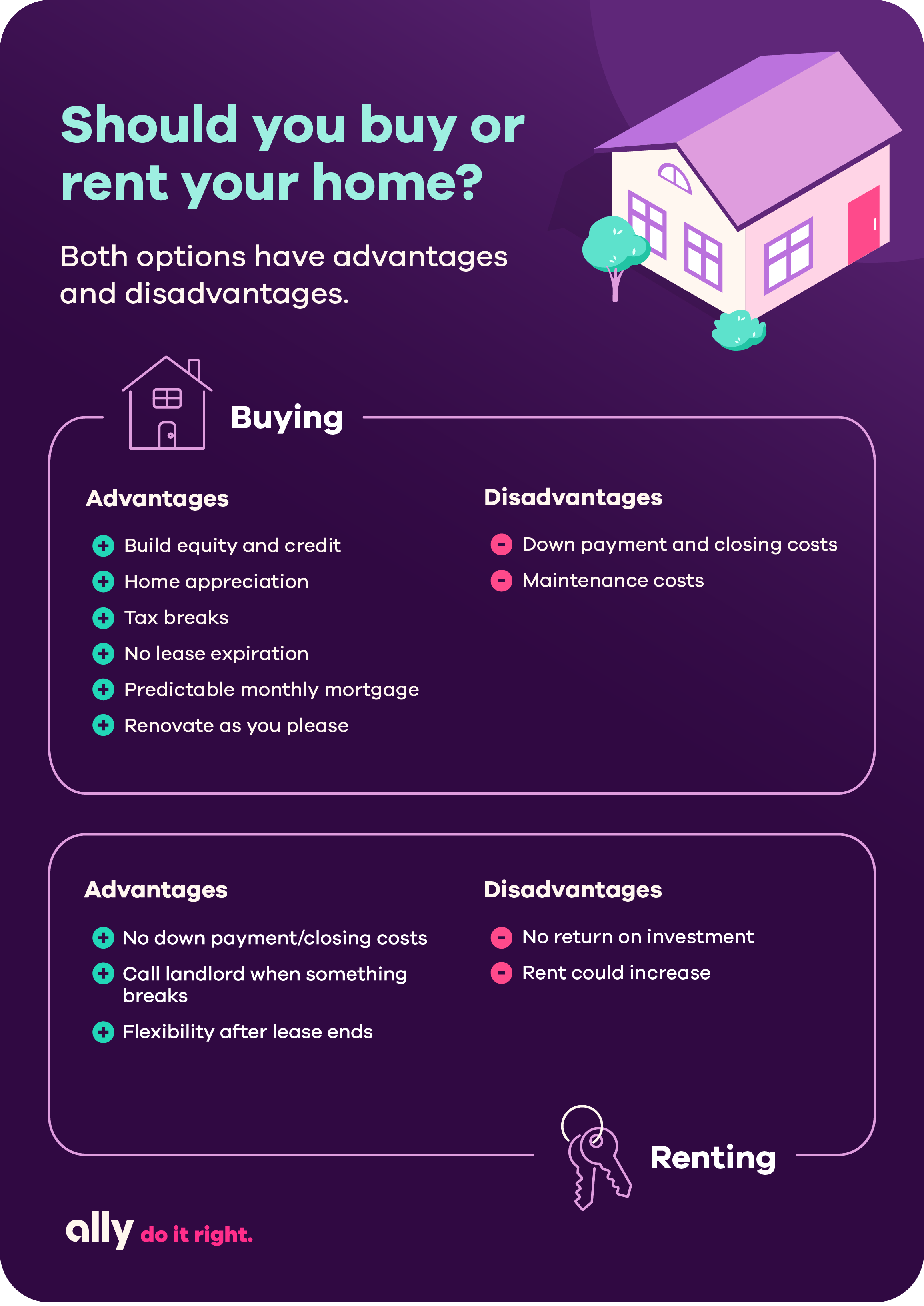

The pros and cons of renting

It's generally more affordable to rent than buy, especially if you consider the true cost of homeownership . Renting also offers flexibility. Without a mortgage, you're only responsible for the rent as long as your lease lasts. Another big advantage of renting is repairs and maintenance are usually taken care of by the landlord or property manager.

On the other hand, when you rent, you don't build equity. Rentals often have restrictions about how much you can change your living space (such as not being able to paint your bedroom walls), and you have to comply with the rules set by your lease. For instance, pets may not be allowed in your apartment.

The pros and cons of buying

As a homeowner, your house (or condo or townhome) is not just a place to live but can be thought of as an investment. That's because with every mortgage payment you make, you build home equity . If you eventually sell the property, the earnings (minus any outstanding balance on your mortgage) are yours.

Your home also will likely appreciate in value over time. If you make improvements along the way, you could recoup even more when you sell. Other factors like population growth, high-demand neighborhoods and market conditions can also drastically affect how your property appreciates.

What's more, you have complete control to modify your living space as you see fit. You can knock down a wall, put in new carpet or make any other changes you wish.

But owning your home comes with a lot of responsibility, too. Any needed repairs and maintenance are on you. Keeping up with lawn care, shoveling the snow and cleaning the gutters can be a big time and/or financial commitment.

As a homeowner, your house is not just a place to live but can be thought of as an investment.

Factors to consider

Whether you should buy or rent comes down to your individual circumstances and preferences. Consider these factors:

The initial cost

In general, if you plan to be at your location for fewer than three to five years, renting may be the way to go. You'll save money on upfront costs associated with buying — like a down payment and closing costs — that you probably wouldn't recoup until many years later (assuming your home appreciates in value). For most rentals, all you need is a security deposit and the first month's rent. But keep in mind, on average, buying a home becomes cheaper if you stay six years or more.

Additional expenses

Beyond those initial costs, the price of unexpected repairs can be a major factor in your decision. Laws vary state by state, but in general, landlords are required to keep properties habitable for renters. If your air conditioner goes out in the middle of summer, your landlord should have it fixed as soon as possible — at no cost to you. And that's big news because an AC unit repair could cost up to $2,000. If you owned your home and needed a new unit, it could set you back around $7,500.

Weigh your options

No matter your financial situation, renting or buying is a big decision to make. Renting may work for you if you're not looking to settle in for the long term and want to avoid large, upfront costs. But buying gives you the ability to build equity and the freedom to make the home improvements you want. Carefully analyze all the angles to make the best decision for you.

Read next

Money solutions and strategies sent straight to your inbox.

Tips and tools to help you build your best financial future.