What we'll cover

How life insurance works

An overview of five common life insurance policies

Pros and cons of different life insurance options

More than 40% of Americans don't think they have enough life insurance. Picking a policy can be overwhelming, so understanding the choices you have, and their advantages and drawbacks, is an important next step in finding the right plan.

How does life insurance work?

Life insurance is a policy where you pay a monthly premium and, in return, your insurance provider ensures your beneficiaries (family, friends, charities) are covered financially when you die. Read more: Supplement your savings with these visualization techniques.

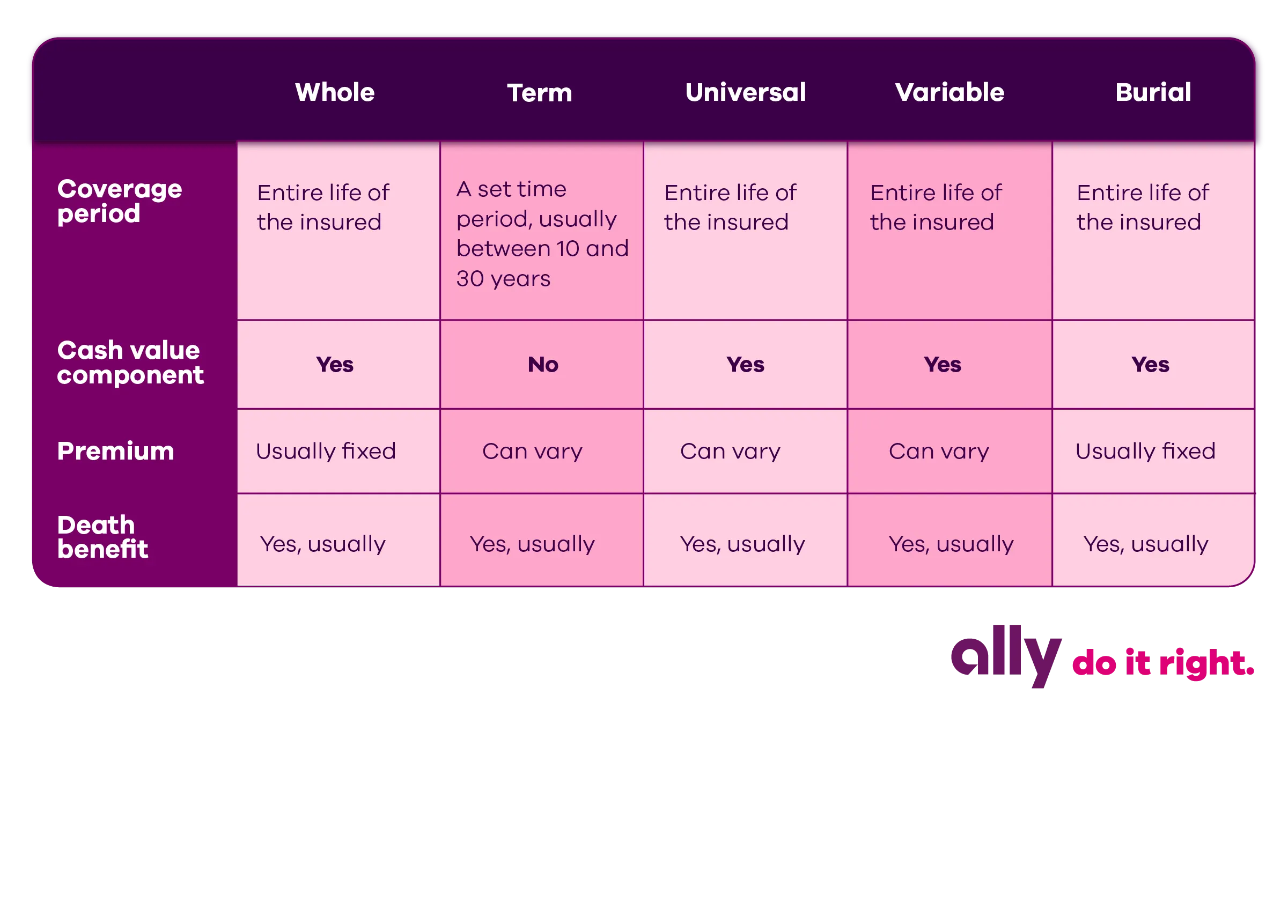

Different types of life insurance

You have a lot of options when choosing a life insurance policy. To help, we've outlined some of the top types and key considerations below.

Whole life insurance

As the name implies, a whole life insurance policy (a type of permanent life insurance) is in effect for your entire life. In exchange for premiums, whole life insurance pays out in two components:

Death benefit: A predetermined sum of money your beneficiaries will receive when you die.

Cash value: The amount that has accumulated based on the percentage of your premiums that has been invested.

Whole life insurance includes a separate investment component that you can borrow against or cash out, with significant caveats. And you have options to access your policy's cash value early, but keep in mind that each comes with consequences and penalties.

Pros and cons of whole life insurance

Longevity is the clear upside. While options like term life insurance only last for a set time period, whole life insurance covers you for the duration of your life. The cash value that comes with whole life insurance is an added benefit as well. But you must weigh that against the additional costs, which can easily be 10 times more expensive than term life insurance. And although it does offer an investment opportunity, its returns will possibly be smaller than those you could receive from other investments, such as a typical 401(k) or individual retirement account.

Term life insurance

Term life insurance is the simplest, and generally most affordable, type of life insurance. The policy is based on a set period of time (aka the term). You pay the same premium on a monthly basis. If you die within that term, your beneficiaries can file a claim to receive a predetermined payout.

Pros and cons of term life insurance

Term life insurance is less expensive than whole life insurance. However, term life insurance has no cash value component, and the policy ends when your term does. If you become uninsurable during that time, you could have difficulty qualifying for another affordable term policy.

Variable life insurance

Variable life insurance is another type of permanent life insurance with a cash value account that is invested in various sub-accounts. These investment choices act similarly to mutual funds but are only available within a variable life insurance policy.

Pros and cons of variable life insurance

Variable life insurance policies can have significant tax advantages, such as tax-deferred accumulation of earnings. You can also access the cash value with a tax-free loan, but unpaid loans reduce the death benefit. And because variable policies are a lot more volatile, you should only consider one if you can tolerate the associated risk. Variable life insurance is more expensive than term and the cash value can grow or decrease based on the performance of the underlying securities in the policy. It does offer some flexibility by letting you pay a smaller amount of the premium based on the cash value. For example, if your premium is $500 per month and your cash value has reached the required amount, you can choose to pay only $250 and use the cash value to pay the remainder.

Universal life insurance

Universal life insurance also has a cash-value component, but it grows based on the current interest rate set by the insurer.

Pros and cons of universal life insurance

This kind of policy shares many of the same advantages and drawbacks of variable life insurance. The main difference is how the cash value is invested and grows. A variable life insurance policy guarantees a cash value, while a universal policy does not.

Burial life insurance

Also referred to as funeral or final expense insurance, burial insurance is a term policy that covers the costs of your funeral, burial and other end-of-life expenses.

Pros and cons of burial life insurance

It's typically easy to get approved for a policy because it doesn't include many of the health-related questions connected to other life insurance options.

Choose the best life insurance for you

Most financial experts will agree that a term life insurance policy is the simplest and most effective way to protect your family, as opposed to more complex and expensive permanent options. But it's important to understand the ins and outs of each option. Use your family's specific needs and personal financial goals as your guide to finding the right fit. Ally Insurance is referring you to Ladder for an innovative approach to term life insurance with an easy online application process and a variety of coverage options to fit a wide range of needs.

Disclosures: Ladder Insurance Services, LLC (CA license # OK22568; AR license # 3000140372) distributes term life insurance products issued by multiple insurers – for further details see www.ladderlife.com. All insurance products are governed by the terms set forth in the applicable insurance policy. Each insurer has financial responsibility for its own products.2203.9-LDRev 3/22