CD laddering: Make this savings strategy work for you

- 5 min read

What we'll cover

-

What CD laddering is

-

How to build a CD ladder

-

Pros and cons of CD laddering

Laddering CDs (certificates of deposit) might sound complicated, but it’s a pretty simple way to help your savings perform smarter for you. With a CD ladder, you can take advantage of the higher rates generally offered by long-term CDs and still maintain regular access to your money.

The basic idea is to open several CDs with staggered maturity dates, so that some of your cash is available to use or rollover at regular intervals. This way, you can take advantage of better rates — usually offered by long-term CDs — without the commitment of having all your money tied up for three-to-five years or more.

What is a CD?

A certificate of deposit (CD) is an interest-bearing deposit account in which you agree to keep your initial deposit for a specified time. A CD has a fixed term length and a maturity date, which can be anywhere from a few months to a few years. When you reach the maturity date, your funds can be withdrawn-penalty-free. Like other deposit accounts, such as checking and savings accounts, CDs are federally insured up to the maximum amount allowed by law when issued by an FDIC-insured institution, such as Ally Bank.

What is a CD ladder?

A CD ladder is built by depositing a sum of money, equally, across multiple certificates of deposit with a series of maturity dates. The length of the CD determines the amount of guaranteed interest; typically, the longer the maturity of the CD, the higher the rate.

The ladder can provide value with the passing of time. As the first CD expires, assuming the cash isn’t needed, the balance (which has grown with interest) can be rolled into the longest-term CD with the highest interest rate. You’re essentially back to where you were on day one, except a portion of your money is earning even more interest than it was before.

This maturing and rolling over continues until, eventually, all CDs in the ladder are in the longest maturity, highest rate CDs, yet expiring in equal, consecutive terms.

How does a CD ladder work?

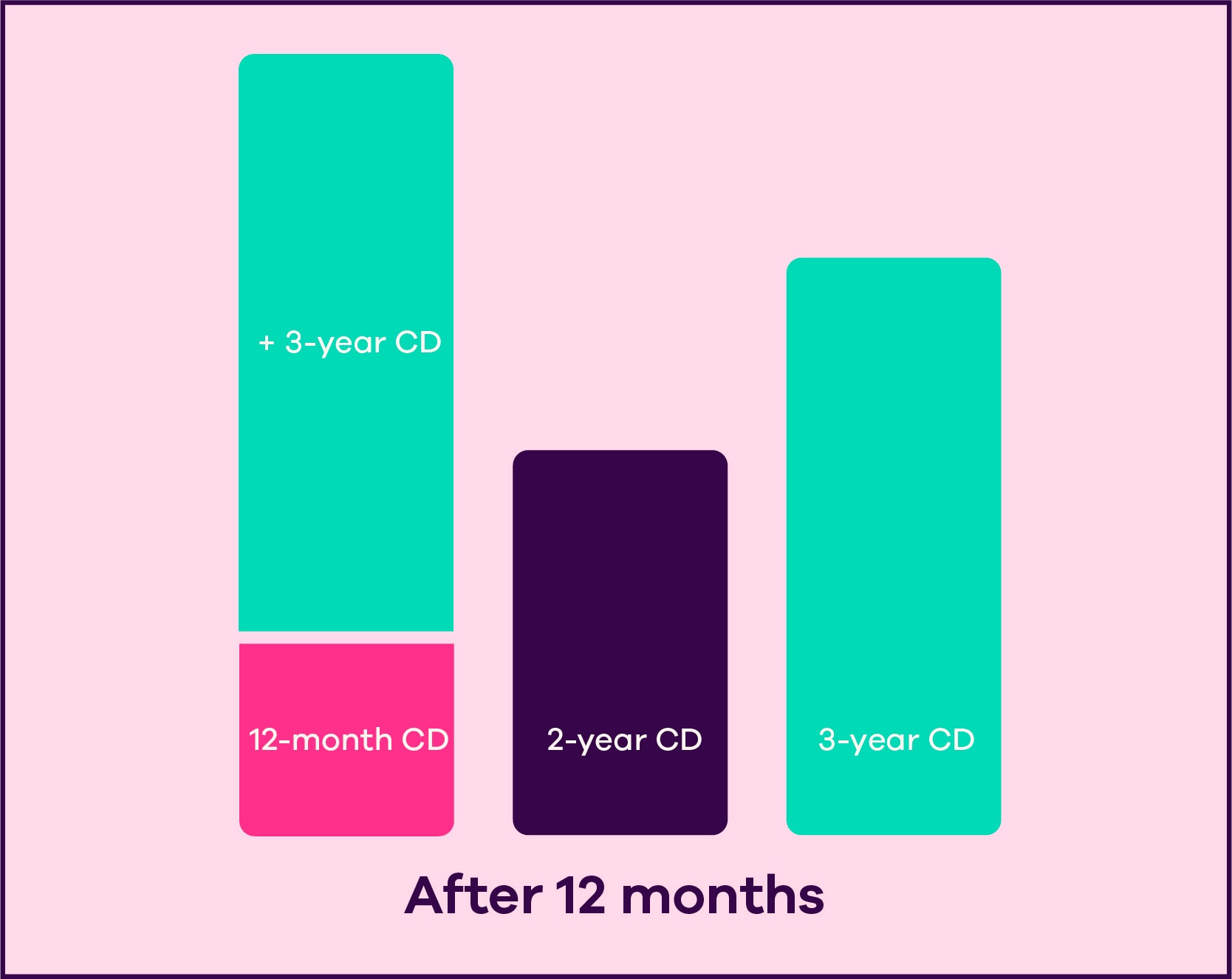

The concept of a CD Ladder strategy can be a bit difficult to understand without visualization, so here’s a chart to help you see how one is built:

Say you have $30,000 and are building a three-year ladder.

You would want to divide the money evenly, so open three CDs with $10,000 each and with ascending terms 12 months apart. Here is how your ladder starts:

When your 12-month CD matures , you can choose to take your money if you need to – or you can keep your ladder going by renewing your CD.

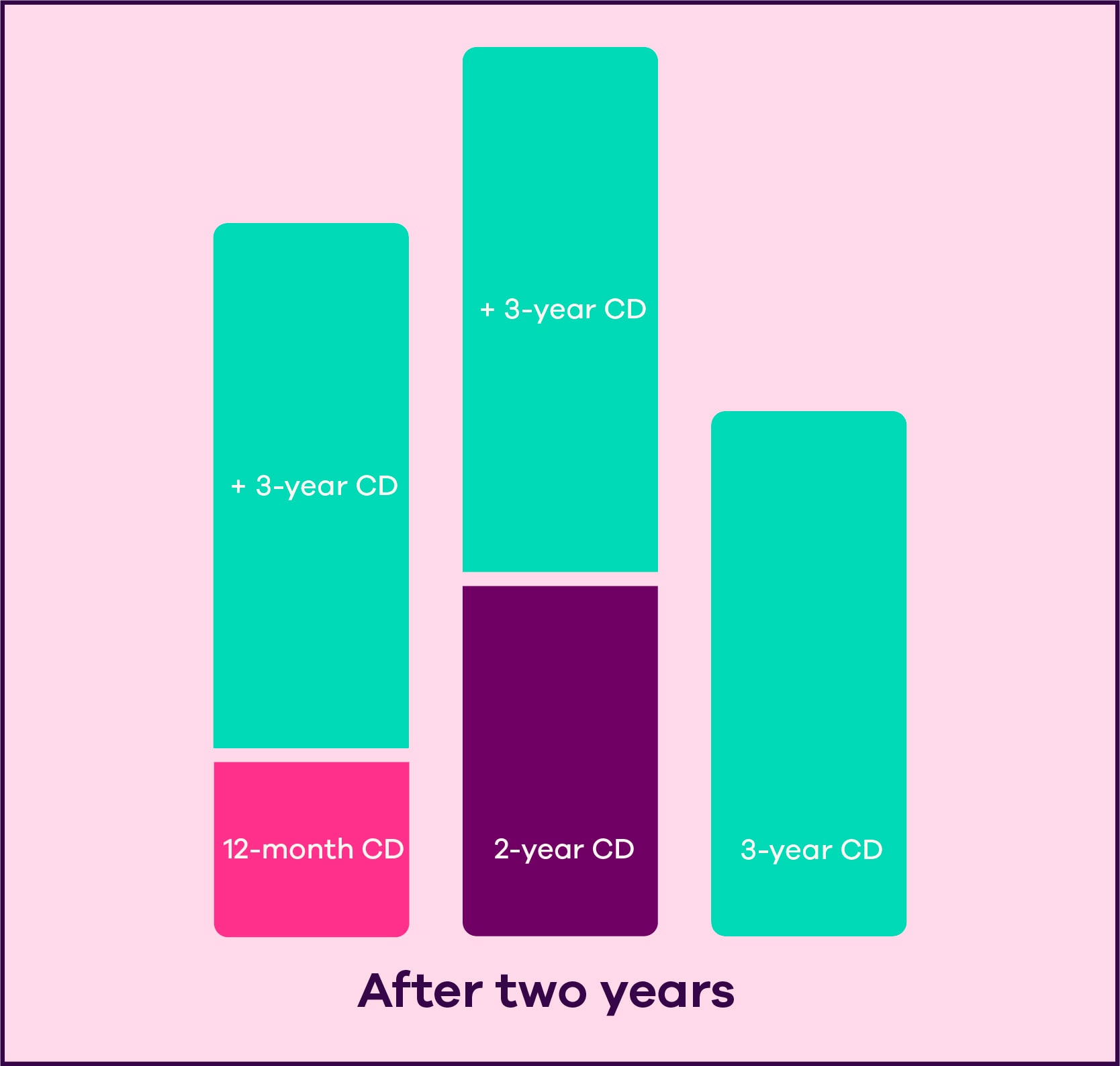

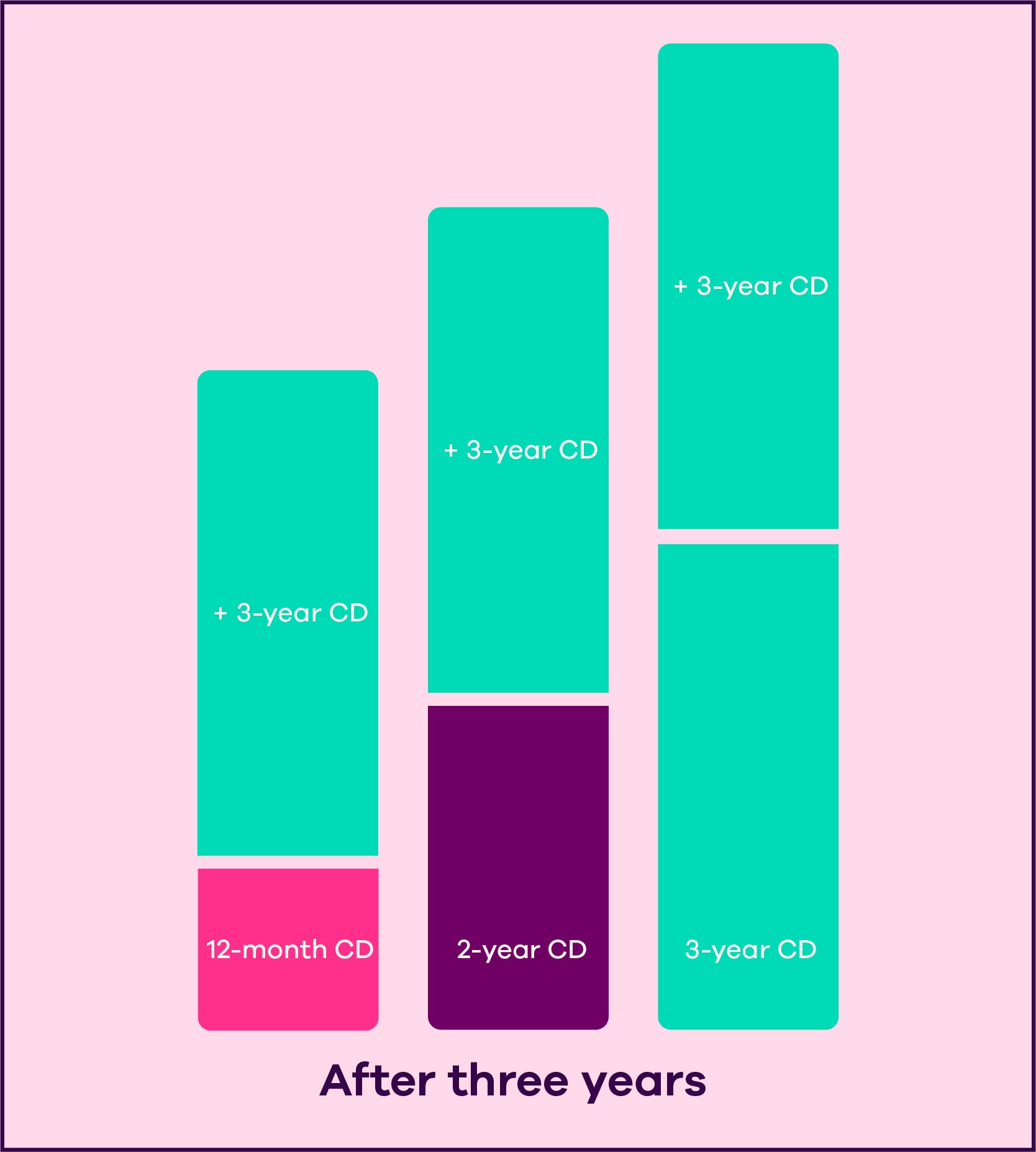

You’ll have the same option after two years.

And again after three years.

But wait, there’s more. Once all the original CDs have been renewed, the ladder is on autopilot, and you’ll benefit from three-year rates while still having access to a portion of your funds annually.

What does this mean for your money? Your earnings are based on your terms and total deposit. Here’s an example: Say you choose a three-year ladder with an initial deposit of $30,000 like the one listed above. If you were to select a 12-month CD at 4% APY, a two-year CD with 3.25% APY and a three-year CD at 4.10% APY, your potential balance would be $37,971 in six years. If you’re looking for a low-risk, reliable return, CDs are a great option.

How to build a CD ladder

The process of creating a CD ladder can be broken down into two main steps:

Step 1: Open the initial CD

Start by opening your first CD account.

Step 2: Renew when CD matures

When your account reaches its maturity date, it’s now time to rollover the balance in the next longest-term CD with the highest interest rate.

Benefits of a CD ladder

This strategy has a number of advantages, including:

Competitive rates

Your CD ladder money can be deposited in higher-interest accounts that can produce, on average, a higher return than a money market or online savings account over the same period of time.

Liquidity and accountability

Access cash at frequent intervals with a ladder compared to one single CD, yet infrequently enough to allow your money to grow.

Provides a barrier to withdrawal

Do you find yourself drawing money out of your savings account a little too often? A CD ladder makes it feel a bit more difficult to access your saved funds and gives that money a time-bound goal.

Diversification and low risk

Laddering your CDs adds diversity to your assets and provides a great option for shy or low-risk savers. Laddering your CDs also provides rate diversity and the ability to capture higher rates as short-term CDs expire.

Peace of mind

Take advantage of interest increases over time with a ladder of CDs, and maintain higher interest if rates fall with older CDs.

Laddering your CDs adds diversity to your assets and provides a great option for shy or low-risk savers.

Drawbacks of a CD ladder

The strategy also comes with some potential downsides, including:

Penalties

Depending on the CD, you might be penalized if you tap into your CDs that haven’t matured yet. Keep in mind that Ally Bank offers a few No Penalty CD options.

The long game

To get the most out of your CDs, you have to play the long game. If you don’t think you can stick it out to capture those higher interest rates, it may be better to stash your cash in a high-yield Ally Bank Savings Account .

Rate changes

Although having predictable rates provides you peace of mind, you might also feel like you missed out if you build your ladder and then rates rise shortly after.

Building your financial future

When it comes to saving for your future, you have a lot of options with varying risk levels. A reliable option like a CD ladder could help you ensure your finances are secure as you build toward your money goals.

Read next

Money solutions and strategies sent straight to your inbox.

Tips and tools to help you build your best financial future.