Many investors wonder if there’s a perfect moment to enter the investment world. But that perfect moment often doesn't exist. Instead of trying to "time the market" — a strategy that's notoriously difficult even for seasoned professionals — it’s often considered more effective to focus on starting early and maintaining consistency over time. This guide will walk you through key principles to navigate your investment journey confidently and strategically.

1. Start investing early

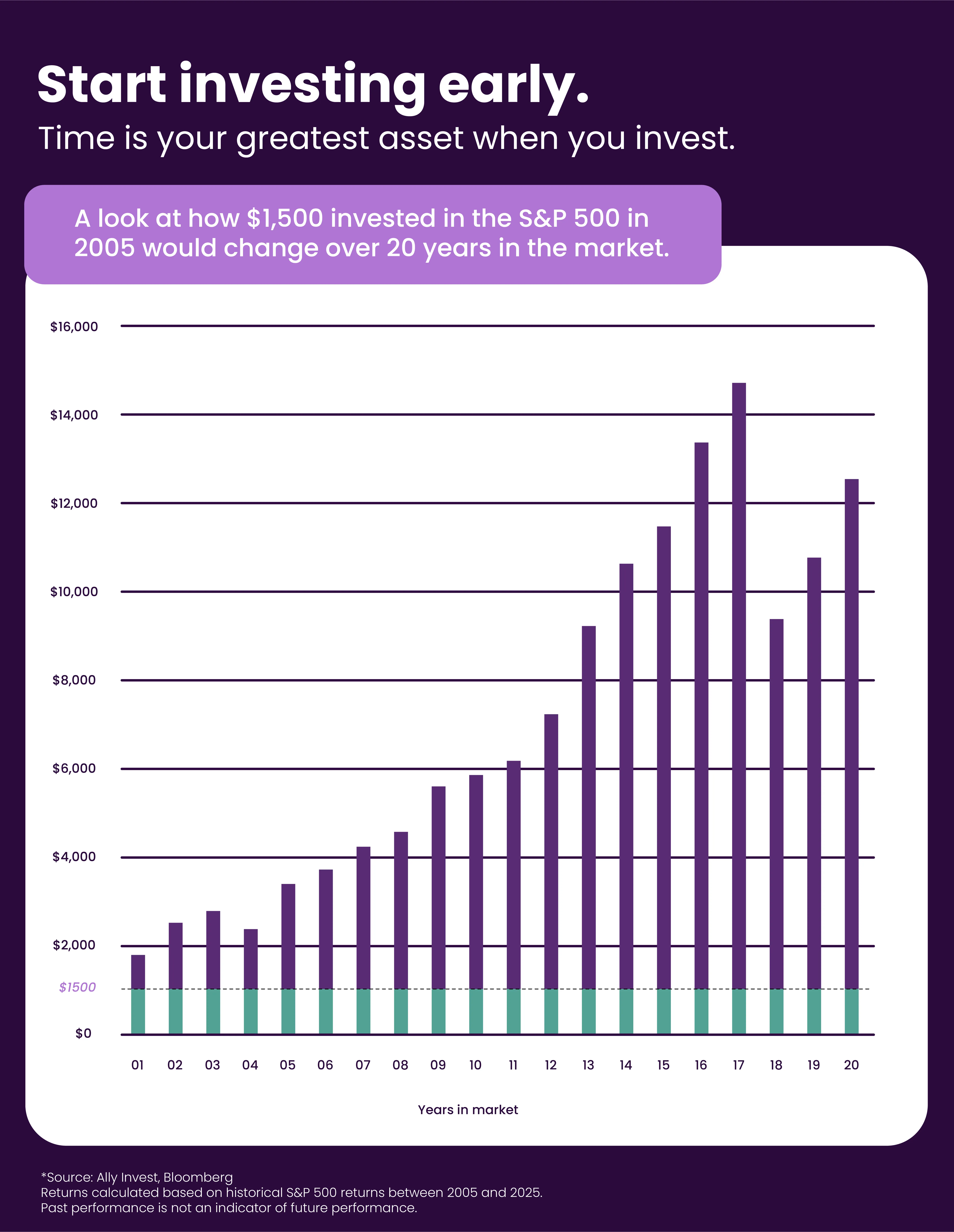

One of the most powerful tools you have as an investor is time. Delaying your entry into investing means potentially missing out on years of market changes. The sooner you begin, the more time your money has in the market.

Let’s look at some historical market trends by tracking how a $1,500 lump sum investment would’ve changed over 20 years if invested in the S&P 500 in 2005.

Historically, markets tend to trend upwards over the long term, despite short-term fluctuations. As we look back at historical S&P 500 returns, we see that longer holding periods have an increased likelihood of positive returns. While past performance doesn't guarantee future results, it underscores the importance of long-term commitment.

It's important to remember: Your resilience as an investor often matters more than the exact day you make your first investment.

Your resilience as an investor often matters more than the exact day you make your first investment.

2. Set clear goals

Before you dive into investing, take time to define what goals you’re pursuing with your money. Clear, well-defined financial goals will serve as your roadmap. Are you saving for retirement, a down payment on a home, your child's education or another significant life event?

Consider these questions as you set your goals:

What is your timeline? Short-term goals (under 5 years) might require different investment strategies than long-term goals (over 10 years)

What is your risk tolerance? How comfortable are you with the possibility of your investment value fluctuating, even temporarily? Your risk tolerance should align with the types of investments you choose, as well as your timeline

How much do you need? Knowing your target amount helps you determine how much to invest regularly

3. Embrace the uncertainty

The investment landscape is dynamic and unpredictable. Not even a seasoned investor can foresee market movements, economic shifts or stock performance. Trying to predict these factors can lead to delayed starts and suboptimal decisions.

Instead of being deterred by uncertainty, understand it as an inherent part of investing. Markets have historically endured and recovered from various challenges. Since 1950, the S&P 500 has averaged over an 11% annual return, navigating through 11 economic recessions, 11 bear markets (drops of 20% or more), and 40 corrections (declines of 10% or more). Being prepared for market volatility means understanding that fluctuations are normal and often temporary in the grand scheme of a long-term investment strategy.

4. Diversify your portfolio

Diversification is a core principle in managing investment risk. It means spreading your investments across various assets, industries and geographies to help mitigate the impact of any single investment performing poorly.

If market swings cause you concern, building a diversified portfolio can offer a sense of security. Here are some examples of what might be considered aggressive vs. conservative.

Aggressive assets: These might include stocks and exchange-traded funds (ETFs) that can invest in a broad basket of stocks. These tend to offer higher growth potential but also come with higher risk

Conservative assets: These could include bonds and exchange-traded funds (ETFs) that can invest in a broad basket of bonds. These are generally considered less volatile and can bring some stability to your portfolio

By diversifying, you acknowledge that different investments may react differently to market events, potentially insulating your portfolio from significant downturns in one area. This strategy doesn't eliminate risk, but it can help smooth the journey, ultimately helping you stay invested through market ebbs and flows.

5. Be consistent

Consistency is vital for any long-term investing strategy. Regular contributions, regardless of market conditions, leverage the power of dollar-cost averaging and compounding.

One effective way to ensure consistency is to set up automated investment transfers. Even small, regular contributions can accumulate significantly over time thanks to compounding, which is the idea that your investment earnings also have earning potential over time. For example, based on historical S&P 500 returns over the last 20 years, consistently investing just $20 a month into a hypothetical, no-fee S&P 500 fund in 2005 would’ve resulted in $1,865 after five years, $5,511 after ten years, and $21,859 after twenty years.

Get started investing today

Taking the step to start investing might seem daunting, but by focusing on these guiding principles, you can build a confident approach to your investing strategy.

You’ve already taken the first step by learning more about different investment strategies. Now, it's time to put these principles into action and begin pursuing the financial future you want.