Trusts have long been thought of as an inheritance tool meant only for the super wealthy, thanks to the “trust-fund baby” stereotype. But in reality, anyone who wants to leave precise instructions on how their assets should be managed after they’re gone can set up a trust.

What is a trust and how does it work?

It’s used to decide how a person’s money is managed and distributed, typically after they die. A trust can hold cash and a variety of financial assets: savings accounts, stocks, property, collectables, other investments — whatever they want to leave to their beneficiaries.

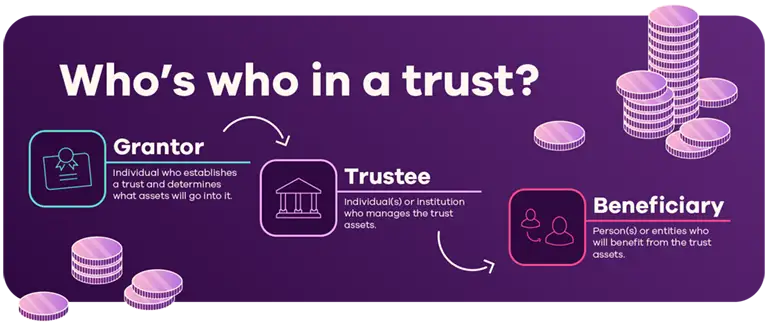

Three key parties involved in a trust

These roles can be filled by one person or by different individuals and entities:

Grantor: Creates the trust and funds it with assets.

Trustee: Manages the assets according to the grantor's instructions.

Beneficiary: Receives the trust's benefits.

Types of trusts

All trusts are one of two types: Revocable or irrevocable.

Revocable vs. Irrevocable trusts

With a revocable trust, the grantor controls the trust’s assets during their lifetime. They can add to or remove property from the trust, change its beneficiaries and even dissolve it. Since assets in revocable trusts are still considered the grantor’s property, they continue to pay taxes on the income generated by the trust assets, and the trust assets are still considered part of the grantor’s estate for estate tax purposes.Irrevocable trusts are less flexible, and modifying or dissolving it can be much more difficult. In addition, irrevocable trust assets are generally no longer considered part of the grantor’s estate and any income or capital gains taxes owed on trust assets are paid by the trust. By removing assets from the grantor’s estate, an irrevocable trust can help reduce or avoid estate taxes at the grantor’s death.

Specialized trusts

When it comes to trusts, grantors can get as specific as they want:

Living trust: A way to manage assets during the grantor’s lifetime and avoid the lengthy probate process after their death

Special-needs trust: A legal arrangement that holds and manages assets for a person with a disability, without disqualifying them from needs-based government benefits

Charitable trusts: When assets are transferred to a trustee for the benefit of a specific charitable purpose, often providing tax benefits

Benefits of establishing a trust

Estate planning advantages

There are many advantages to a trust, including: [WC1]

Avoiding the public, time-consuming and expensive probate process

Minimizing estate taxes

Providing for loved ones, including minors and those with disabilities

Asset protection

One draw of having a trust is being able to shield assets from creditors and lawsuits. You can also ensure that your assets are distributed according to your wishes.

Disadvantages of a trust

More paperwork

Trusts can be complicated to set up and generally require more time, effort and paperwork than a will, for instance.

Cost

You will need to hire a financial professional or estate attorney to establish the trust, and you may hire an individual, bank or financial institution to manage its ongoing execution as well.

Creditors

If you die and owe debt, creditors can file a lawsuit to collect the debt, which could leave your beneficiaries in an uncomfortable situation.

Trust vs. will

While you can have both a will and a trust as part of your estate planning, they have some key differences. Wills take effect upon the death of the grantor, while trusts can be used both while the grantor is living and after their death. Another major difference is that a will can dictate matters unrelated to finances, such as who will be the guardians of children under 18, or instructions for your funeral and burial; trusts cannot.

Steps to establishing a trust

Interested in setting up a trust? Follow these steps:

Define your objective: Determine what you want to achieve.

Select trustees and beneficiaries: Choose trustworthy individuals or institutions to manage and benefit from the trust.

Work with professionals: Consult financial advisors and attorneys to draft the documents.

Fund the trust: Activate the trust by transferring assets into it.

Review regularly: Ensure the trust remains aligned with your goals and legal requirements.

Ready to take the next steps?

If you’re interested in exploring a trust, consult with a professional. Then explore our guide to see if opening an Ally Bank Spending Account, Ally Bank Savings Account or certificate of deposit (CD) in the name of your trust is right for you.