Cash is often crowned king — and for good reason. It typically upholds its value and allows you to instantly make purchases. When you add cash into an account or investment, it's also important to understand how easily you can access it, which is known as liquidity.

Read more: How Ally Bank’s Spending and Savings Account work together to optimize your finances

What is financial liquidity?

Financial liquidity refers to the ease with which an asset — anything ranging from a money market savings account to an ETF to real estate — can be converted into cash relatively quickly.

Types of liquidity

While several classifications exist (for example, funding liquidity), the main types are:

Market liquidity: How easily an asset can be bought or sold in the market without causing substantial price changes.

Accounting liquidity: A company's ability to meet short-term obligations, like bills or payroll, with its liquid assets.

Why is liquidity important?

Everyone's motives for having cash readily available may be different and can vary over time. But you'll likely have moments in life where you need cash on-hand, whether it's accessible funds for an emergency, the ability to capitalize on timely investment opportunities or even to limit your exposure to market volatility. An asset that cannot be quickly converted into cash without a significant loss of value is considered an illiquid asset. Examples include collectibles and fine art, real estate and collectible luxury items.

Measuring financial liquidity

You can use several different ratios to assess liquidity:

Current Ratio: Current assets divided by current liabilities.

Quick Ratio (Acid-Test Ratio): (Current assets - Inventory) divided by current liabilities.

Cash Ratio: Cash and cash equivalents divided by current liabilities.

Factors affecting market liquidity

Market liquidity can be unpredictable and impacted by many factors, including:

Economic conditions: Market stability can influence liquidity levels. For example, high volatility can decrease liquidity as investors become uncertain and move towards safer assets.

Market sentiment: Investor confidence impacts asset liquidity. Positive sentiment usually increases trading activity (improving liquidity), while negative sentiment can lead to panic selling (reducing liquidity).

Regulatory changes: Policies and political crises can alter liquidity dynamics in financial markets.

Examples of liquid and illiquid assets

Some assets are highly liquid, while others have far less liquidity. The degree of liquidity is often determined by regulations and required processes, for example, a stock can usually be sold more quickly than a real estate transaction due to the required steps, as well as the market and demand.

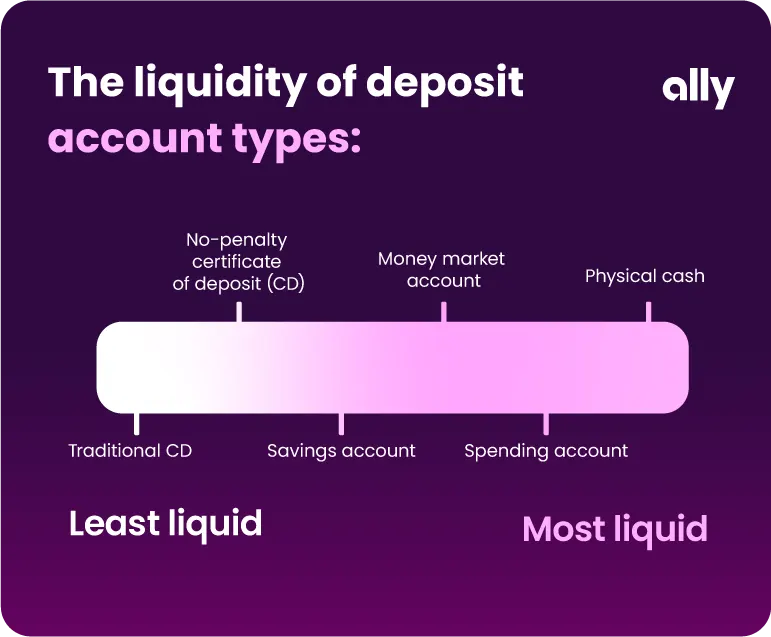

The liquidity of deposit accounts

The liquidity of deposit accounts varies by account type. Here’s what to know about each:

Checking and Money Market accounts: Accounts like an Ally Bank Spending Account or Money Market Account typically come with checks and debit cards so you have nearly instant access to your funds.

Savings accounts: Accounts like an Ally Bank Savings Account also provide a level of liquidity, but with a few key differences. Although you can't directly withdraw from a savings account with checks or debit cards, you can take advantage of free transfers (up to a predetermined amount per statement cycle) to either a linked checking account or money market account.

Certificate of Deposit (CD): These interest-bearing bank accounts typically come with an early withdrawal penalty charge if you choose to withdraw your funds before the maturity date (aka the end of the CD's term). A good alternative solution is an Ally Bank No Penalty CD, which allows you to enjoy competitive interest rates and withdraw your total balance any time after the first six days of funding your CD, penalty-free.

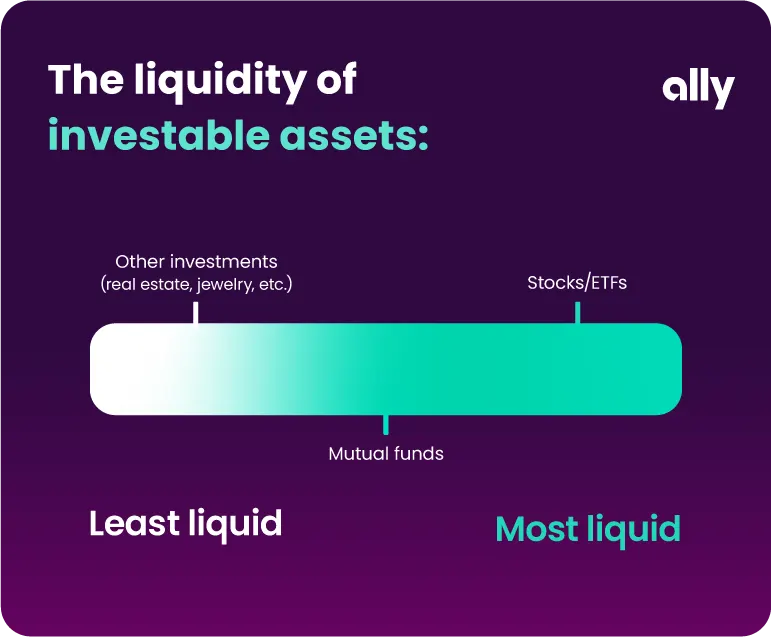

The liquidity of investment types

Some investment types are highly liquid, while others have far less liquidity. Keep in mind, the liquidity of stocks and ETFs depends on market activity and investor demand. Large, actively traded securities tend to be more liquid, while those with lower volume can be more illiquid. Mutual funds do not have intraday liquidity like stocks or ETFs and are only priced once per day. An Ally Self-Directed Trading Account could be utilized to trade these securities.

Other non-security investments are not traded on a public exchange and are typically the least liquid. It can include a business, real estate and even collectible items like art or rare coins. Because it can take several steps to sell these types of investments, extra time is typically needed before you receive any cash in exchange.

Before you invest, you should carefully review and consider the investment objectives, risks, charges, and expenses of any mutual fund or exchange-traded fund (ETF) you are considering. ETF trading prices may not necessarily reflect the net asset value of the underlying securities. A mutual fund/ETF prospectus contains this and other information and can be obtained by emailing support@invest.ally.com.

Choosing your liquidity

The good news is you have plenty of deposit account types and investment choices to choose from when factoring in liquidity. A good rule of thumb is to diversify your portfolio and always allocate your funds based on your individual preference, risk tolerance and personal goals.